Three Big Questions from Matthew Ball's "The State of Video Gaming in 2025"

What questions could possibly remain after digesting Matthew Ball's gargantuan industry treatise dissecting all angles of the games industry in painstaking detail? Turns out, at least three big ones.

Introduction

In case you missed it, Matthew Ball recently made headlines when he released “The State of Video Gaming in 2025” — a 221-slide behemoth of data, analysis, and compelling observations that diagnoses how the games industry came to be in its present state of tumult and attempts to identify potential sources of future growth.

If you’re not familiar with Ball, he is the multihyphenate author of 2022’s “The Metaverse: And How It Will Revolutionize Everything.” He’s been pumping out thought-provoking treatises on all manner of topics covering media and entertainment for years. Avid readers of Always Scheming will know that I am a frequent consumer of his oeuvre.

After mustering the courage (and caffeine) required to read through the entirety of the report1, I decided to consolidate it into a handy Twitter thread for easy perusal:

The majority of the report is backwards-facing, dissecting each major segment of the games industry in detail to paint a picture of how and why the sector faces so many challenges today: layoffs, game cancellations, commercial failures, VC pullback, and so on.

It’s a multifaceted set of issues, but Ball does his best to sum it up in a single run-on sentence for the TL;DR crowd:2

If you want all the gory details, you’ll find them in the Twitter thread above. Be warned: it gets bleak at times. Many have criticized the report as being overly dour; I prefer the term “realistic.”

Today, we’ll focus on the forward-looking parts of Ball’s report, which is where astute readers will likely find the greatest sources of optimism.3

Specifically, Ball offers up several potential sources of future growth:

After reading Ball’s analysis and thinking through the ramifications, I was left with three major questions. They don’t cover all of the “growth engines” Ball identifies (again, I encourage you to check the Twitter thread for the full breakdown), but they will give us plenty to think about as we begin a new year in search of growth for the games industry.

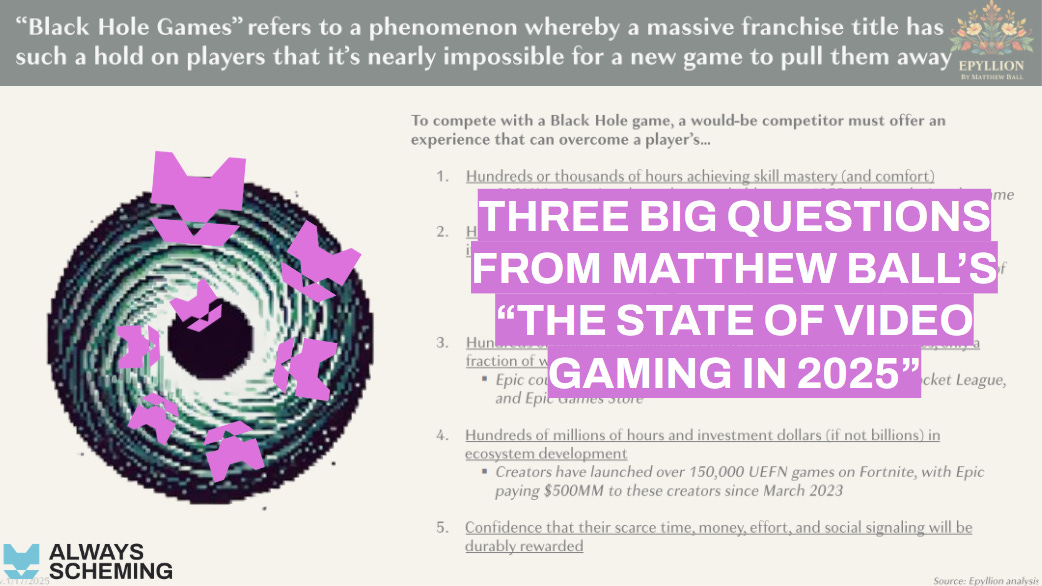

Question #1: Who Benefits from Industry Growth?

I suspect a major reason that Ball’s report was received harshly in some circles of the games industry is not due to the alarming set of facts laid bare, but rather because of what those facts portend for both consumers and (most) industry participants.

Many of the potential growth drivers Ball has identified are totally reasonable. It’s hard to argue that companies won’t try to earn more money from advertising, drive efficiencies through AI adoption, or raise prices further to combat inflation. But try explaining to the average gamer that these changes are going to be a boon for the industry. Consumers don’t care about growth; they already feel like they’re being nickel-and-dimed by most publishers.

Similarly, many industry operators are likely nonplussed by Ball’s proposed growth drivers. Unless they happen to work at one of the few companies identified as key beneficiaries (Valve, Nintendo, Roblox, Discord) or operate one of the so-called “Black Hole Games,” most developers will continue to face a tough competitive landscape.

To be fair to Ball, these issues are really beyond the scope of his document. Ball’s concern with a report like this is industry-wide growth; it doesn’t much matter to him where that comes from, or if it’s heavily weighted towards a select few beneficiaries.

Indeed, “Fewer Games & Studios” is one of the nodes in Ball’s Vicious Cycle slide, wherein he describes what will happen to the industry without new growth drivers. Winner-takes-most outcomes certainly play into that.

Further, if you believe that increased adoption of AI will drive production efficiencies and lower costs, it would be fair to assume that existing Winners could potentially take more of the pie while utilizing an equal or lesser amount of resources to do so. “Black Hole Games” thus become even more difficult to compete with.

On the other hand, another potential outcome would be a broader stratification of the games industry, where an emerging “luxury” class (something Joost van Dreunen has previously hypothesized) drives the consumption of higher-priced titles, while the middle- and lower-class audience bears the brunt of increased advertising. I don’t know if this is any better or worse than the scenarios outlined above (or even mutually exclusive), but it feels increasingly likely.

Question #2: How much can we infer about “non-core” markets from the data about China?

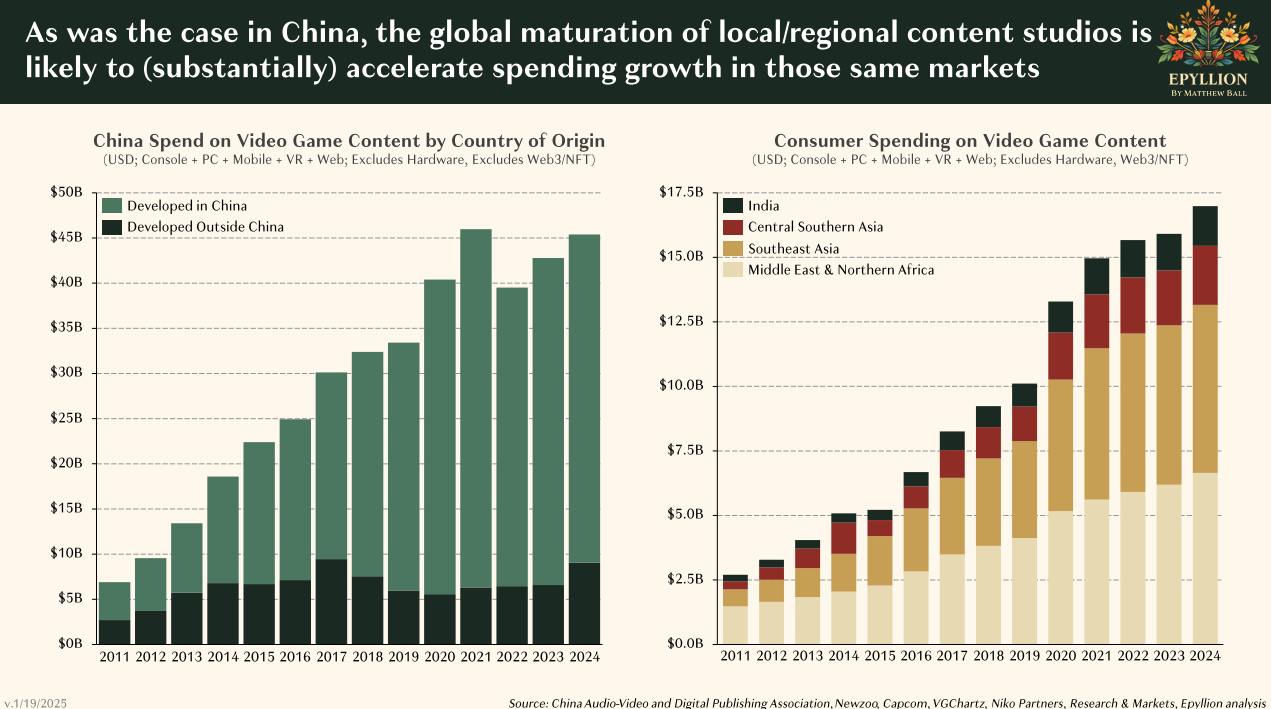

Ball spends several slides examining the data on China: its large and growing share of the PC segment, its contributions to broader industry growth over the last several years, and the idiosyncratic nature of its games market. Specifically, Ball shows that Chinese gamers spend almost exclusively on Chinese (i.e. domestically produced) games, while Chinese companies manage to simultaneously capture a huge share of revenue from non-Chinese gamers, too.

He then draws on data from the Chinese, Nigerian, and Indian film industries for evidence that “non-core” markets may increasingly redirect spend towards local productions, as opposed to Western imports. While the examples are from film, the implication is that the same could occur in gaming. As “non-core” markets improve their game development and publishing capabilities, Ball posits, those markets will rapidly accelerate their own spending growth (thereby contributing to overall industry growth).

I think there are three potential issues raised by this line of thinking.

First and most glaringly is that China’s media market is unlike that of any other major country in that it is tightly controlled and regulated by the Chinese government. The PRC approves games and films for domestic consumption and will capriciously ban any titles that don’t fit its agenda.

The Chinese games industry is simply not on a level playing field with its overseas peers. This state of affairs could be thrown further into flux during the new Trump administration; just take a look at what’s happened with ByteDance and Tencent in recent days. Either way, drawing a throughline from China to other nations is not as straightforward as one might assume it to be, based solely on the data presented.

Interestingly, Ball spends several slides discussing the preponderance of Chinese-speaking Steam users. What’s not mentioned, though, is that Steam occupies a sort of gray market in the PRC. Steam users in China must either use a censored version of the app or utilize a VPN to get access to the full Steam library. To be clear, I’m not disputing the data4, but I think it’s worth pointing out that, again, China is a unique market.

The second issue I’d raise would be whether we can truly make such direct comparisons between film and games on this specific topic.5

I agree with the notion that deeper localization and culturalization of games will naturally attract greater domestic engagement and spend. However, I question the ease with which “non-core” markets will be able to build up their own domestic game development and publishing capabilities.

My assumption (key word!) is that it will take many, many years for a given “non-core” market to develop the local talent and expertise necessary to generate meaningful industry-expanding revenues from domestic-facing games — far longer than it might take for that same country to achieve similar results from a domestic-facing film industry.

Furthermore, even if local expertise were no issue, these markets are home to extremely low ARPU6 audiences. Just because the games are targeted at local players does not mean that those players will have money to spend on those games.

Finally, the third issue that comes to mind is that there seems to be an unspoken assumption of cultural preferences in “non-core” markets, though it’s hard to say whether its an English-speaking thing, or a broader Western nations vs. Rest-of-World divide. Whatever the case may be, there is a key assumption that “non-core” markets creating homegrown games for domestic audiences is somehow more effective than importing games made in “core” markets.

Put differently, if Chinese prefer Chinese games and Koreans prefer Korean games and Americans prefer American games (never mind the fact that we just discussed how China is already capturing huge spend from overseas markets), should we not expect that same pattern to hold true elsewhere? Do French gamers prefer French games? What about Mexicans? Turks? Swedes?

Perhaps it comes down to our definition of “core” vs. “non-core,” but the data is mixed on this. Japan, for example, is a country that has always had strong local preferences for its own games; 2024 was no exception. On the other hand, eight of the ten PC/Console chart toppers in Europe for 2024 were made by American firms. In India, 2024’s highest grossing mobile games came from companies based in Singapore, China, Israel, USA, Japan, and Finland.7

I recognize that stating “each market has its own distinct preferences” is not a profound observation, but I’m not yet convinced that “non-core” markets will be a meaningful driver of industry growth over the next three to five years.8 I could, however, easily see that changing over the longer term.

Question #3: Does web3 still have a role to play?

Outside of identifying it as a would-be “growth engine” that has thus far failed to deliver, Ball spends little time discussing the role of web3 and blockchain-enabled gaming in his analysis.

I don’t blame him — the sector has been plagued with scandals, has failed to deliver hits, and has generally been more talk than substance. Reading the fine print on Ball’s industry-wide charts, you’ll notice that he explicitly “[e]xcludes Web3/NFT” in all of them.

Blockchain gaming is tough to quantify with the same sort of rigor that Ball applies to other sectors. The segment is loosely defined, spans multiple platforms, and has all sorts of attribution challenges. While some firms have tried to quantify impact — such as Helika's attempts to show that web3 gamers monetize at higher ARPU rates — most industry reports rely upon vanity metrics like “games announced” or “unique active wallets” to forward their agendas.9

However, as an optimist on the topic of blockchain-enabled games myself, I can’t help but wonder what the impact might have been if properly quantified. I’m not under any illusions that it would significantly move the needle, but I would be curious to see web3 revenues deduplicated and stacked on top of the other sectors. Would it be more substantial than, say, AR/VR (~$1-$2B)?

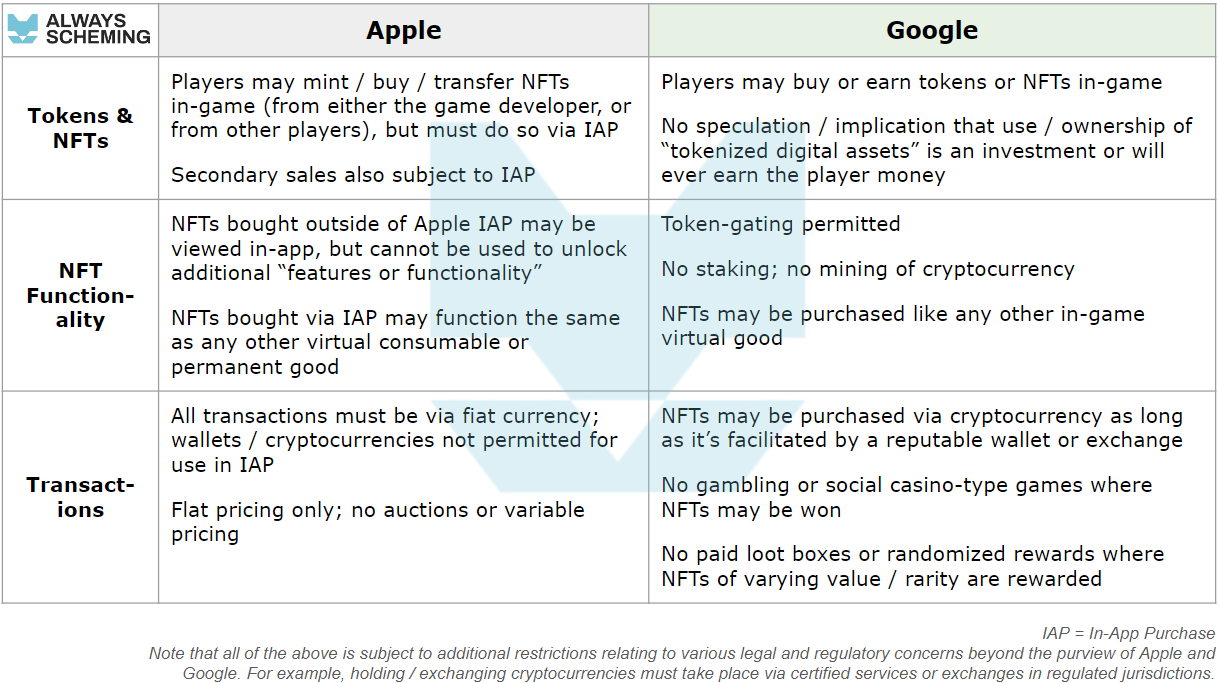

Though Ball doesn’t mention web3 as a potential growth driver,10 it’s worth reconsidering the possibility in the context of four other catalysts that he does mention: “App Store Regulation,” “New Game Genres,” “AI,” and “UGC Platforms & Tools.”

An opening up of app stores to more web3-enabled games and integrations could encourage (or at least not actively prevent) new experiments in game design, monetization, and fundraising from the blockchain gaming crowd. It would also open up critical distribution channels that are currently restricted or (in the case of Steam) blocked outright.

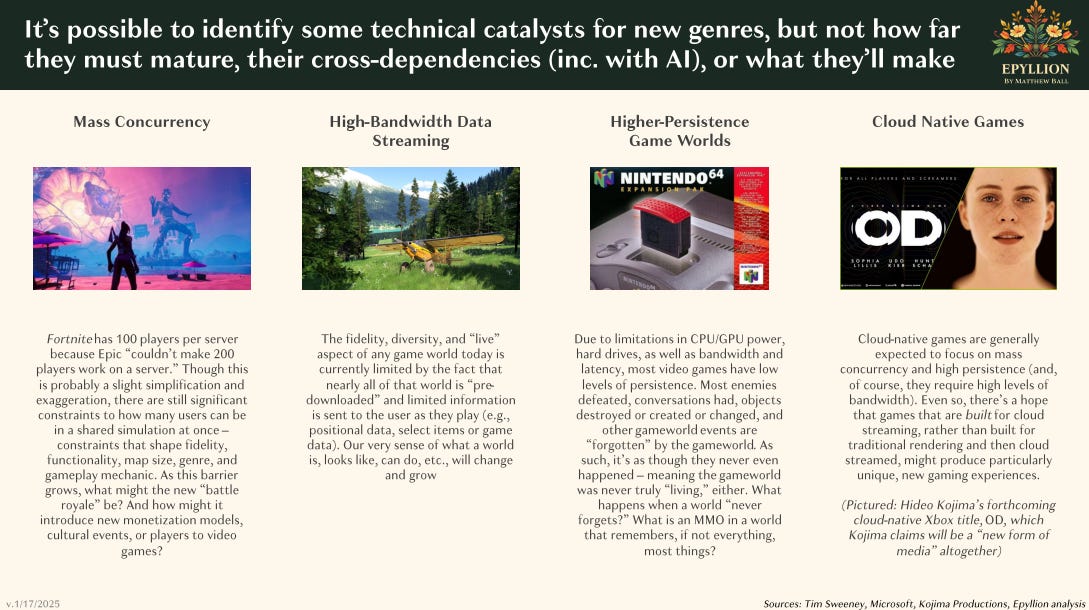

As Ball argues in both his “New Game Genres” and “AI” sections, a confluence of maturing technologies can unlock new experiences for players that may have previously been infeasible or wholly unattainable. I won’t rehash the arguments about what blockchains bring to gaming here, but if you believe (as I do) that web3 can be additive, then there’s no reason to exclude it from the list of potential “technical catalysts” alongside AI and the many others Ball mentions.

Ball also mentions companies seeking to expand their offerings beyond the boundaries of games themselves. He specifically cites EA’s new EA Sports App as an example of this. The “Crypto x AI” intersection is already transcending the borders of individual applications via proto-games like Freysa. With AI agents increasingly being integrated into crypto games, the experience of the “game” itself quickly expands to communication channels, social media, financial markets, and other platforms.

These are the sorts of experiments that drive much-needed innovation. Will they lead to industry growth? Who knows. In the short term, probably not. Beyond my personal interest in these types of experiences, I bring them up only to emphasize that they fit the same descriptions Ball applies to more “traditional” gaming companies in his report.

As readers of Always Scheming will know, I write another newsletter focused on the fully onchain games space.11 Within that niche (and across web3 more broadly), the idea of a permissionless UGC ecosystem is frequently discussed. Some view it as a reason to be optimistic about blockchain games; others believe that UGC offers a potential business model for web3, aligning creator and player incentives in a more equitable and efficient manner than existing standards.

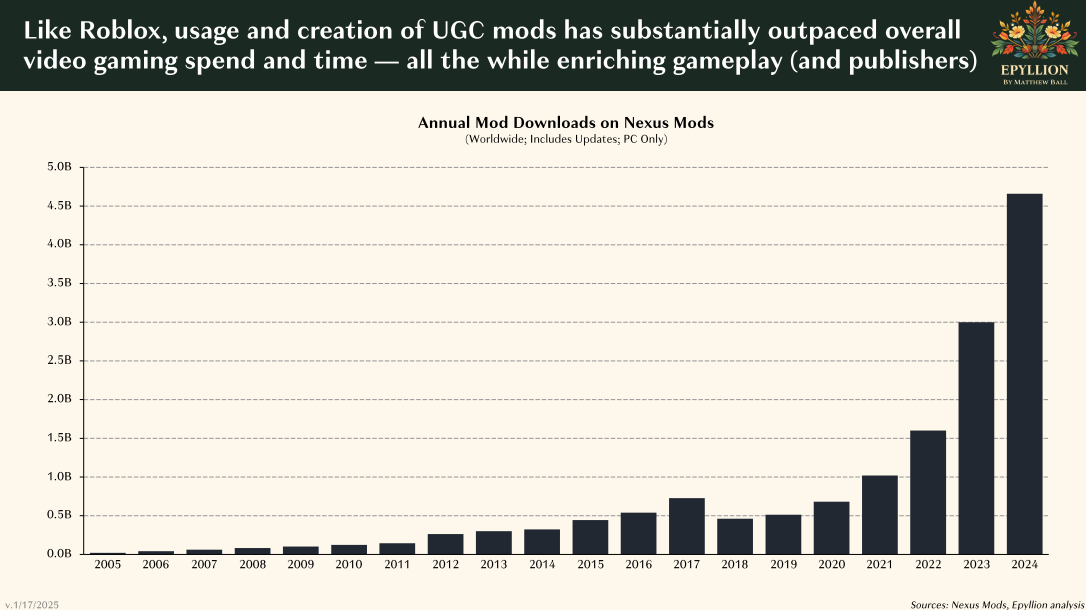

Ball also discusses UGC ecosystems at length, though most of his analysis is dedicated to Roblox. What caught my attention, though, was his discussion of mods. We all know the story by now: battle royales, MOBAs, auto-battlers, and many of the largest and most successful games ever created can trace their humble origins to the modding community. Indeed, Ball shows how the use of mods has grown rapidly in the last several years.

However, the less optimistic note for web3 advocates is that flourishing modding ecosystems require more than just a permissive community: they need a hit game. Ball’s data shows that the largest modding communities congregate around the biggest games. Until blockchain gaming has a breakthrough on the level of Baldur’s Gate 3, Fallout 4, or Stardew Valley, any predictions of UGC-as-savior-business-model will likely remain unfulfilled.

In Conclusion

So many of the reactions to Ball’s report on social media have been, frankly, braindead. If you consider yourself a savvy consumer of data, as I do, consider avoiding the LinkedIn comment threads on this topic.

A lot of the criticism seems to originate with indie developers and other “true gamers” upset about the perceived exclusion of perspectives from smaller creators. Much of it boils down to some form of the following:

“What about [My Favorite Game X]?! That game was a hit in 2024! The whole report must be BS if it missed that obvious data point!”

Aside from these being anecdotal observations, they are almost entirely inconsequential to the overall market, which is Ball’s fundamental concern with this report.12

Ultimately, regardless of your perspective, the report is just data (albeit a whole lot of it). Use it or ignore it as you see fit, but if you ask me, any serious operator should be thinking deeply about the implications of this report.

Do yourself a favor and set aside some time to dig into the full deck. You’ll be smarter for having done so and will be better prepared for the year to come.

Perhaps ironically, Matthew Ball’s company is called “Epyllion,” which is defined as “a relatively short narrative poem resembling an epic in theme, tone, or style” (Merriam-Webster). Many phrases might be used to describe Ball’s writing, but “relatively short” is not one of them.

Call me crazy, but I think this probably could have come just a bit earlier than Slide 114.

Though it’s certainly not optimistic for all parties, as we’ll soon discuss.

Though it’s worth mentioning that the analysis is based specifically on the choice of Chinese language as Steam’s default setting, which could feasibly include a large chunk of the non-Mainland Chinese-speaking diaspora in other territories, too.

Ball makes comparisons to films, books, and other forms of media elsewhere in the report, too. Most of are these are perfectly acceptable, in my opinion.

“Average Revenue Per User”

According to Sensor Tower. Note that this is mobile only, as I couldn’t find a reliable source covering the entire market. India is largely a mobile-first games market; according to Niko Partners, mobile accounts for 77.9% of games revenue, vs. 14.5% for PC and 7.7% console.

Unless, of course, we’re considering China a “non-core” market, too.

If you have a good data source on this, please send it my way!

How far down the list of priorities must it have been to not make the cut in a 221-slide deck?

It’s called Dark Tunnels. You should definitely check it out.

Note also that Ball specifically calls out several indie games as promising new franchises / studios (Slide 125).